S&P 500 — US Large Cap Index

S&P 500 — US Large Cap Index FTSE 100 — UK Blue Chips

FTSE 100 — UK Blue Chips Euro Stoxx 50 — Eurozone Leaders

Euro Stoxx 50 — Eurozone Leaders DAX 40 — German Equities

DAX 40 — German Equities CAC 40 — French Market Index

CAC 40 — French Market Index Nikkei 225 — Japan Benchmark

Nikkei 225 — Japan Benchmark Hang Seng — Hong Kong Index

Hang Seng — Hong Kong Index Shanghai Composite — China Mainland

Shanghai Composite — China Mainland ASX 200 — Australian Market

ASX 200 — Australian Market TSX Composite — Canada Index

TSX Composite — Canada Index Nifty 50 — India Large Cap

Nifty 50 — India Large Cap STI Index — Singapore Market

STI Index — Singapore Market KOSPI — South Korea Index

KOSPI — South Korea Index Bovespa — Brazil Equities

Bovespa — Brazil Equities JSE Top 40 — South Africa Index

JSE Top 40 — South Africa Index IPC Index — Mexico Market

IPC Index — Mexico Market

The Swedish audio distribution platform, listed on a U.S. exchange, fell more than 10% after publishing its Q1 2026 results. Despite the extreme market reaction, the figures do not seem to justify it – at least not at first glance.

- Earnings per share (EPS) came in clearly above expectations, reaching as much as €3.45 versus market expectations of around €2.95.

- Revenue was merely solid, almost exactly in line with the consensus, totaling €4.53 billion.

Additional positives for the company include:

- Premium subscribers increased by 9% year over year to 293 million—close to market expectations.

- Revenue from premium users rose by 10% year over year to €4.15 billion.

- Monthly active users increased to 761 million—also above expectations.

- Gross margin rose to a record 33%, beating the company’s own guidance.

- Operating profit was also record-high, rising to €715 million with a 15.8% margin.

- Free cash flow (FCF) was record-high as well, at €824 million.

Could anything spoil such strong results? The market seems to be focusing almost exclusively on guidance. The company announced that Q2 operating profit is expected to reach €630 million. That is a decline versus Q1 and materially below market expectations of about €674 million. Revenue is expected to increase to €4.8 billion, with monthly active users rising to 778 million.

This suggests the company is not expecting a structural deterioration in business conditions, but rather signaling a temporary dip in profitability – albeit from a very high base. At the same time, the company is showing it can steadily grow revenue, and the user metrics are also providing reasons for optimism. While a significant quarter-on-quarter drop in profitability is a notable short-term issue, the magnitude of the sell-off appears, in the context of this release, overdone.

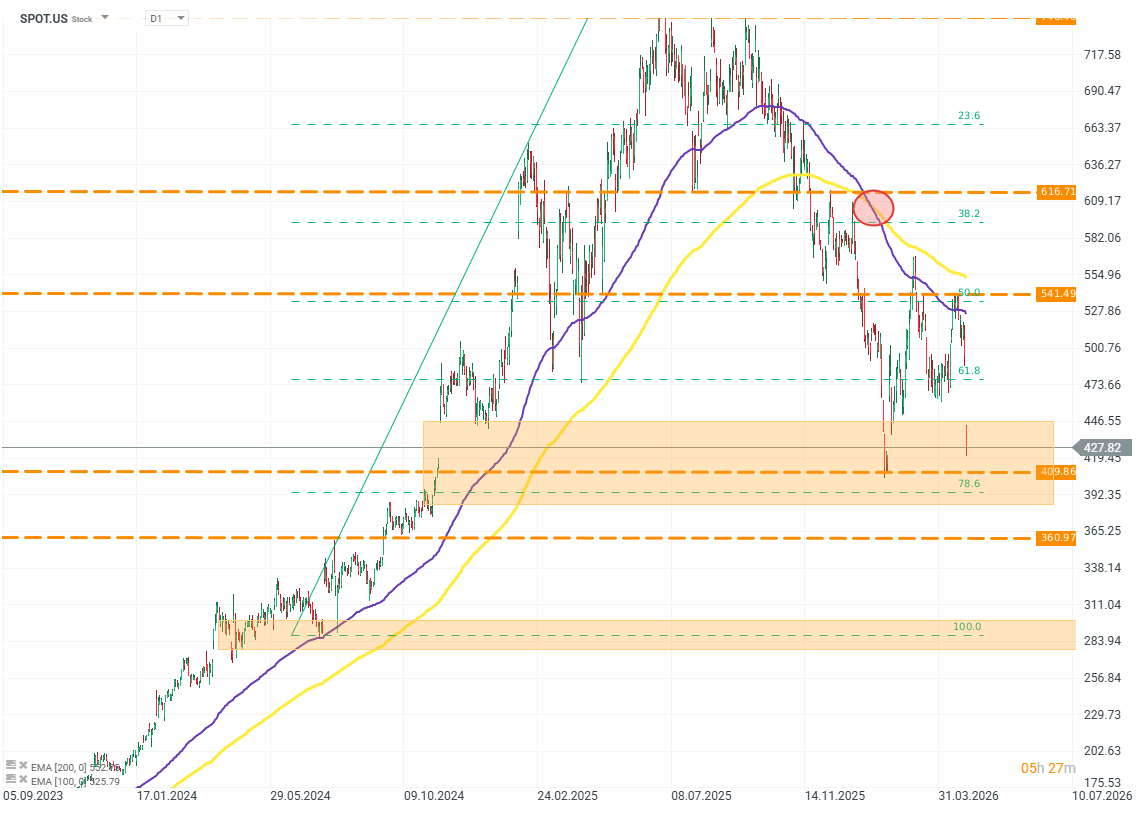

SPOT.US (D1)

The second half of 2025 proved very difficult for Spotify. The company’s valuation fell by as much as 45%, wiping out the entire gain from early 2025. The depth of this decline may raise questions—questions shared by analysts at investment firms. Given the time frame, the drop in the company’s valuation may have been driven mainly by capital rotating into AI-focused companies. Source: xStation5