S&P 500 — US Large Cap Index

S&P 500 — US Large Cap Index FTSE 100 — UK Blue Chips

FTSE 100 — UK Blue Chips Euro Stoxx 50 — Eurozone Leaders

Euro Stoxx 50 — Eurozone Leaders DAX 40 — German Equities

DAX 40 — German Equities CAC 40 — French Market Index

CAC 40 — French Market Index Nikkei 225 — Japan Benchmark

Nikkei 225 — Japan Benchmark Hang Seng — Hong Kong Index

Hang Seng — Hong Kong Index Shanghai Composite — China Mainland

Shanghai Composite — China Mainland ASX 200 — Australian Market

ASX 200 — Australian Market TSX Composite — Canada Index

TSX Composite — Canada Index Nifty 50 — India Large Cap

Nifty 50 — India Large Cap STI Index — Singapore Market

STI Index — Singapore Market KOSPI — South Korea Index

KOSPI — South Korea Index Bovespa — Brazil Equities

Bovespa — Brazil Equities JSE Top 40 — South Africa Index

JSE Top 40 — South Africa Index IPC Index — Mexico Market

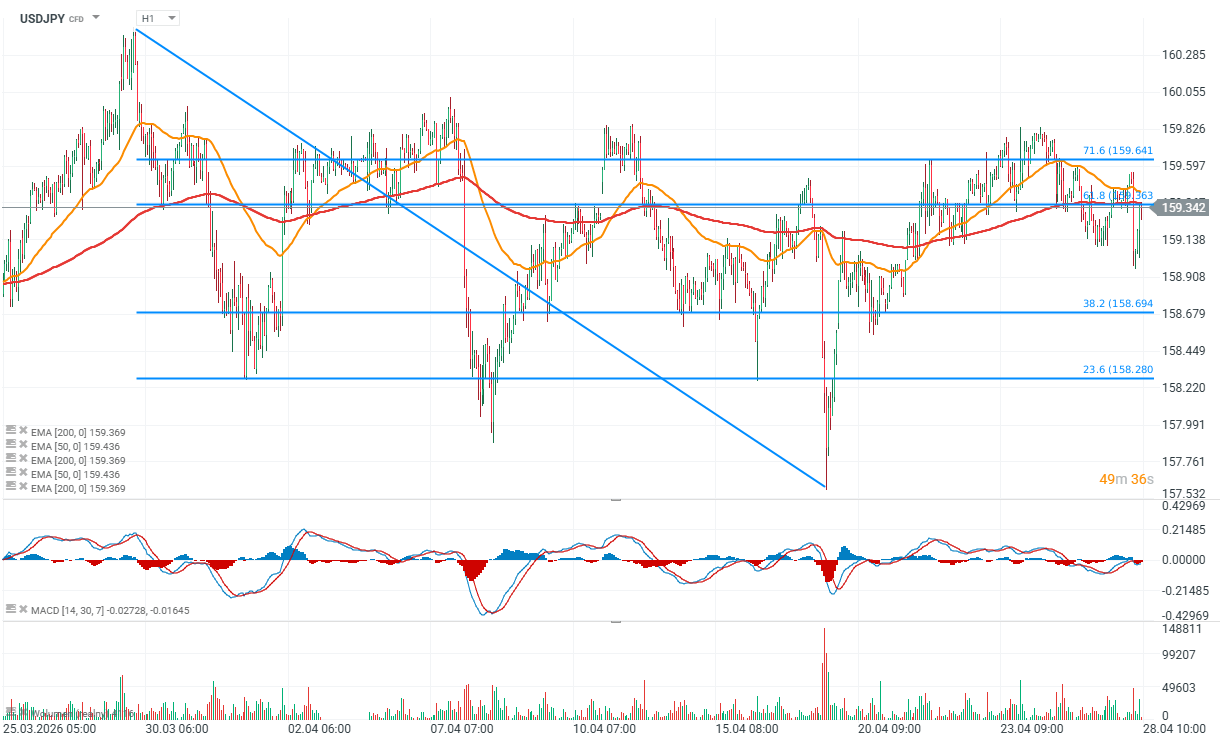

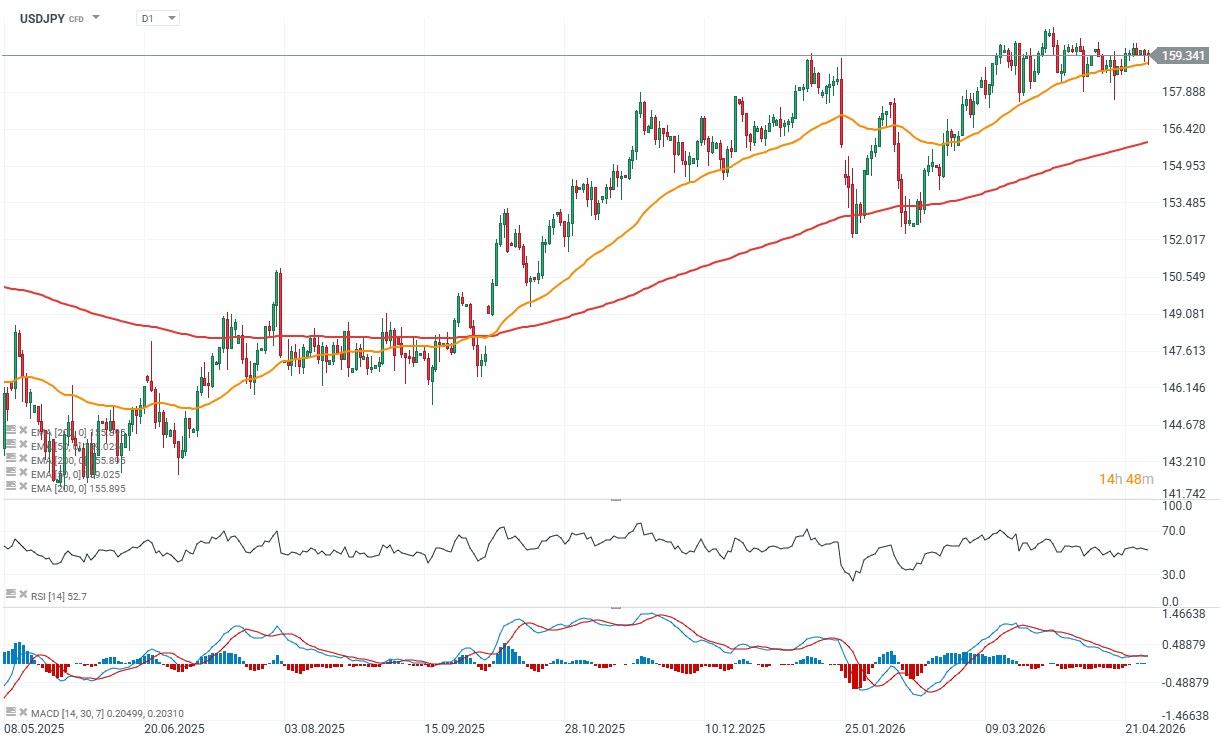

IPC Index — Mexico MarketChart of The Day – USD/JPY with mixed reaction to cautious Bank of Japan decision. Is stagflation heading to Japan?

The Bank of Japan kept interest rates unchanged at 0.75%, in line with market expectations, although the reaction of the USDJPY pair to the decision appears rather mixed. Bank of Japan (BoJ) Governor Kazuo Ueda spoke at a press conference, explaining the reasons behind maintaining the key interest rate at 0.75% during the April meeting. Rate hikes will continue in line with developments in the economy and inflation, with particular attention paid to the impact of the situation in the Middle East. The goal remains to achieve a stable 2% inflation rate, although Japan’s economic growth is expected to slow in 2026. Higher oil prices are likely to reduce corporate profits and households’ real income, although the economy will be supported by government measures such as fuel subsidies.

Key takeaways from the BoJ conference

The situation in the Middle East remains uncertain. Japan’s economy is recovering moderately, although some signs of weakness are visible. Economic growth is likely to slow in fiscal year 2026 due to developments in the Middle East. Close attention must be paid to how these developments affect financial markets, FX markets, as well as Japan’s economy and prices. There is also a need to carefully monitor the risk of inflation deviating significantly to the upside, which could negatively impact the economy. Real interest rates remain at very low levels. The BoJ will continue to raise rates and adjust the degree of monetary accommodation depending on economic activity, prices, and financial conditions. The timing and pace of adjustments will be assessed in the context of the impact of Middle East developments and the likelihood of achieving the baseline scenario. The decision was made by a 6–3 vote, with Nakagawa, Takata, and Tamura dissenting, as they proposed raising the rate to 1%.

Board members’ remarks

Tamura suggested including a statement that underlying inflation is in line with the target, while Takata proposed noting that CPI has already reached the target level. Both proposals were ultimately rejected. Additional comments Oil prices may have a stronger impact on inflation than before. The Bank needs more time to assess the effects of the Middle East situation. Underlying inflation is currently slightly below 2%. It is difficult to determine when the next rate hike will occur. Monetary policy will be conducted in a way that avoids falling “behind the curve.” The decision to hold rates reflects a lower probability of the baseline scenario being realized. The dissent of three board members highlights the difficulty of conducting monetary policy under current conditions. There is no immediate need to raise rates, but they may become necessary if supply shocks generate secondary effects. The risk of rising inflation could be a reason for rate hikes, though not the only one.

BoJ Quarterly Outlook Report

Real interest rates remain very low. Underlying inflation is expected to reach levels consistent with the 2% target in the second half of fiscal 2026 and in 2027. Risks to economic growth are tilted to the downside, while risks to inflation are tilted to the upside. Economic growth is expected to slow in 2026 but should moderately accelerate from 2027 onward. Rising oil prices are expected to affect both CPI and incomes.

BoJ forecasts Core CPI

- 2026: 2.8% (previously 1.9%)

- 2027: 2.3% (previously 2.0%)

- 2028: 2.0%

Real GDP

- 2026: 0.5% (previously 1.0%)

- 2027: 0.7% (previously 0.8%)

- 2028: 0.8%

Key risks highlighted by the BoJ

The BoJ noted that rising oil prices may now pass through more easily into the prices of goods and services than in the past. There is also a risk of stronger increases in food prices, particularly if higher raw material costs feed into production costs. The Bank pointed to the possibility of significant disruptions in global supply chains, which could materially affect the production activity of Japanese firms. The report also addressed artificial intelligence. Strong corporate investment in AI could support the global economy, but if it is not matched by profit growth, it may lead to adjustment pressures in asset markets. The BoJ also emphasized that exchange rate movements now have a greater impact on inflation than in the past, while trade policies implemented so far have partly altered the course of globalization. Medium- to long-term inflation expectations are rising moderately. USDJPY charts (H1, D1)

Source: xStation5

Source: xStation5