S&P 500 — US Large Cap Index

S&P 500 — US Large Cap Index FTSE 100 — UK Blue Chips

FTSE 100 — UK Blue Chips Euro Stoxx 50 — Eurozone Leaders

Euro Stoxx 50 — Eurozone Leaders DAX 40 — German Equities

DAX 40 — German Equities CAC 40 — French Market Index

CAC 40 — French Market Index Nikkei 225 — Japan Benchmark

Nikkei 225 — Japan Benchmark Hang Seng — Hong Kong Index

Hang Seng — Hong Kong Index Shanghai Composite — China Mainland

Shanghai Composite — China Mainland ASX 200 — Australian Market

ASX 200 — Australian Market TSX Composite — Canada Index

TSX Composite — Canada Index Nifty 50 — India Large Cap

Nifty 50 — India Large Cap STI Index — Singapore Market

STI Index — Singapore Market KOSPI — South Korea Index

KOSPI — South Korea Index Bovespa — Brazil Equities

Bovespa — Brazil Equities JSE Top 40 — South Africa Index

JSE Top 40 — South Africa Index IPC Index — Mexico Market

IPC Index — Mexico MarketU.S. energy and utilities sectors in focus 🔍 What will S&P 500 companies show?

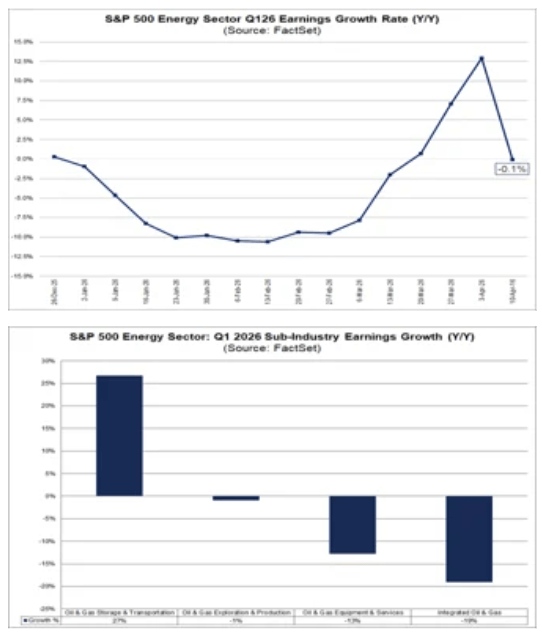

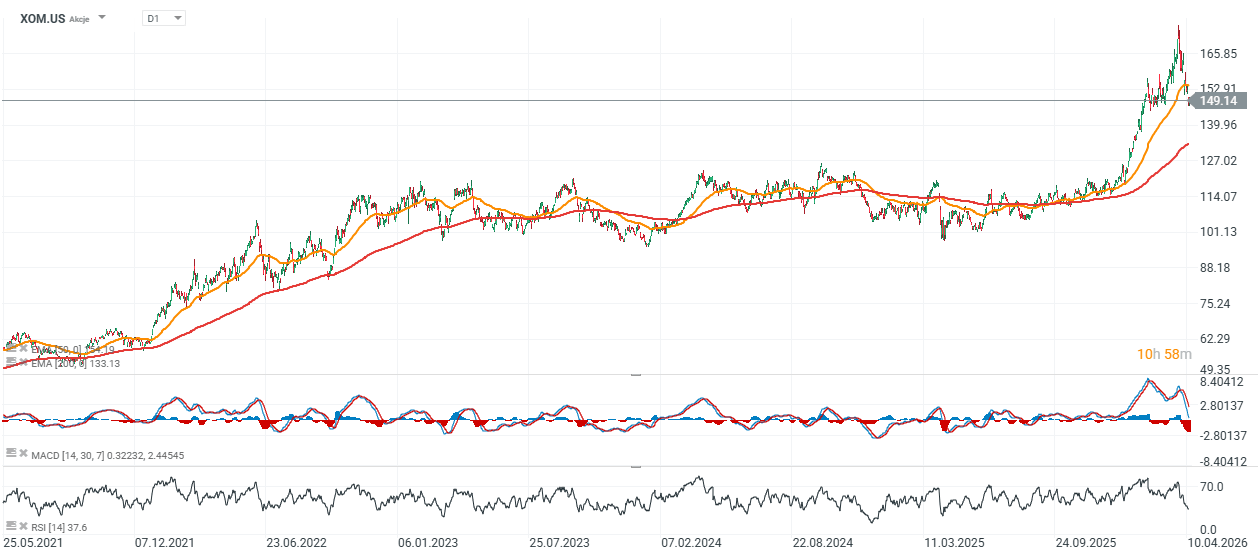

The start of the Q1 2026 earnings season highlights a clear divergence between the Energy and Utilities sectors within the S&P 500. In Energy, a tension persists between a supportive oil price environment and deteriorating expectations for some of the largest companies. Utilities, by contrast, remain one of the more stable segments of the market, benefiting both from their defensive characteristics and from structurally rising electricity demand. Energy companies The Energy sector is currently expected to be one of the weakest in the index in terms of year-over-year earnings growth, with a projected decline of 0.1%. The sector’s outlook has been materially impacted by downward revisions for Exxon Mobil, which is now the primary contributor to the expected earnings contraction. Excluding Exxon, the sector would be posting solid earnings growth, suggesting the weakness is concentrated rather than broad-based.

- Refining, marketing, and midstream infrastructure are currently the strongest segments, benefiting from improved market conditions. In contrast, integrated oil & gas, oilfield services, and upstream companies are showing weaker performance.

- While rising oil prices support sentiment, the average price of crude for the quarter was only slightly higher than a year ago, limiting the positive impact on earnings.

- Geopolitics remains the key variable. The sustainability of elevated oil prices will depend on developments in the Middle East and their impact on supply and export infrastructure.

- At the same time, producers are maintaining capital discipline, with no meaningful shift in production or capex plans, indicating that the current price environment is not yet viewed as a structurally higher regime.

- Medium-term expectations remain strong, with the market anticipating a significant acceleration in earnings growth in the coming quarters.

The escalation of tensions in the Middle East pushed WTI crude above $100 per barrel for the first time since 2022, providing a direct boost to revenues for oil-weighted E&P companies—an effect likely to be visible in current earnings. This contrasts with gas-focused producers, where pricing remains relatively stable despite a temporary spike during Winter Storm Fern. LNG export demand in the U.S. is constrained by high utilization, while storage levels remain close to the five-year average. Despite elevated prices, the durability of the oil rally remains uncertain and largely dependent on the trajectory of the conflict. It is therefore not clear whether higher prices will translate into sustained profitability for major oil companies. The extent of potential damage to critical infrastructure—such as oil fields, pipelines, and export terminals—will be decisive for supply dynamics and price sustainability. Although modest production growth in the U.S. is expected later this year, it is premature to characterize the current environment as a sustained high-price cycle. As a result, companies are likely to stick to existing production and capex guidance rather than aggressively revising plans upward.

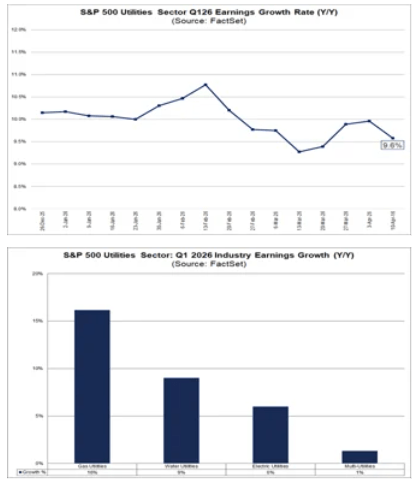

Source: FactSet Utilities companies The Utilities sector enters the earnings season with one of the stronger growth profiles in the S&P 500, with expected earnings growth of 9.6% year over year. Compared to Energy, this growth is more stable and broadly distributed, with all major industry groups expected to contribute.

- Independent power producers and renewable-focused companies are performing particularly well, although meaningful contributions also come from gas, water, and electric utilities.

- In the near term, the sector benefits from its defensive characteristics, but increasingly from structural demand growth for electricity.

- A key driver is the expansion of data centers and AI-related infrastructure, which is expected to increase system load and support investment in grid capacity and generation.

- At the same time, the sector operates in a more uncertain regulatory environment, particularly in offshore wind.

- Rising political risk around offshore wind may lead to a reallocation of capital toward natural gas and LNG, implying a more pragmatic—but less “green”—energy transition.

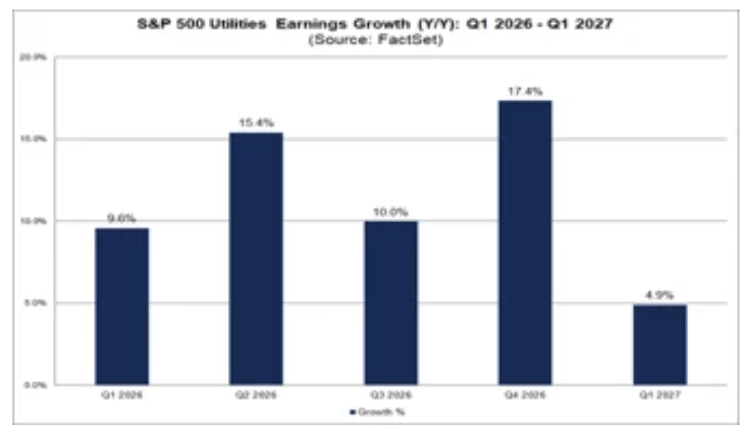

- From an investor perspective, Utilities remain one of the more predictable segments of the market, offering relatively stable earnings growth in the coming quarters.

Since the beginning of the Trump administration, offshore wind projects have faced significantly increased uncertainty. Lease sales and permitting in federal waters were halted early on, followed by stop-work orders for projects under construction. Although courts later blocked these measures, the outlook for new leasing activity remains limited in the near term. After construction resumed, projects such as Revolution Wind and Coastal Virginia Offshore Wind began delivering power, while Vineyard Wind completed turbine installation. Regulatory uncertainty has also begun to drive capital reallocation. A $928 million agreement between the U.S. government and TotalEnergies will see the company exit offshore wind leases in exchange for reinvesting in LNG and Gulf of Mexico oil production. The Department of the Interior has since initiated discussions with other leaseholders on similar arrangements. If replicated more broadly, this could accelerate long-term investment in natural gas. Such a shift would support near- and mid-term electricity demand growth—particularly from AI infrastructure—while slowing the development of offshore wind, previously seen as a cornerstone of long-term energy transition.

Source: FactSet The Energy sector remains primarily driven by oil prices, revisions for major companies, and geopolitical risk. Utilities, on the other hand, are increasingly becoming an exposure not only to defensiveness but also to long-term growth in electricity demand and the evolving energy mix. For the market, this distinction is critical: Energy is characterized by volatility and selectivity, while Utilities are gaining importance through predictability and the quality of their growth profile. XOM.US, D1 interval

Source: xStation5

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.