President Donald Trump’s address on April 1, 2026, directed to the American nation and broadcast from the White House during prime time, was intended to calm global financial markets and outline a path out of the escalating conflict with Iran. However, the reality proved quite the opposite. The speech not only failed to answer key questions but sowed even more uncertainty, resulting primarily in a resurgence of rising oil prices—a factor that shapes sentiment across all financial markets and carries immense significance for the global economy. Donald Trump’s appearance demonstrated that the United States lacks any concrete plan for the current conflict with Iran; there are no clear prospects for reopening the Strait of Hormuz, threatening a global energy paralysis that the world and financial markets seem unwilling to acknowledge. Everyone continues to hope that the conflict will end overnight and that the price of a barrel of oil will return to the $60–$70 range seen before the start of the war.

Nevertheless, Donald Trump spoke a few words that warrant attention. The crucial element of the speech was not the tough declarations about ending the war or striking hard, but rather what the President did not say: the total lack of a plan for the physical unblocking of the Strait of Hormuz and the silence regarding the potential use of ground forces to secure key transit points.

In the absence of concrete solutions, volatility surged across markets once again. Oil prices are rebounding by as much as 8 per cent, and prices could potentially close at their highest levels since the conflict began. Although short-lived optimism, triggered by earlier signals of a possible end to military operations, boosted stock indices during the day, the content of the address—or rather the lack thereof—caused a return to falling precious metals prices, a sharp retreat in Asian stock indices, a drop in Wall Street futures, and a strengthening of the US dollar in the wake of high oil prices.

Investors have realized that the Trump administration is operating in a strategic vacuum, assuming that the Strait of Hormuz will “open itself” the moment American forces withdraw—a notion experts consider extremely unrealistic and dangerous wishful thinking. While the market still fails to see the risk, we are potentially facing the greatest energy crisis in history, and momentarily, every country in the world will rush into a war for resources.

What did Trump omit in his address?

An analysis of the content of President Trump’s speech points to a deliberate avoidance of the most pressing technical and military issues. Although the President announced that “major strategic objectives are near completion,” citing the degradation of Iranian missile and drone systems, he ignored the fact that Iran still retains the capability to asymmetrically block shipping through water mining, fast motorboat attacks, and the use of the terrain along the coast. The market expected a clear plan for escorting tankers or an international coalition to secure the route; however, Trump shifted the responsibility to third countries, stating that nations dependent on the strait “must take care of this passage themselves.”

The lack of mention of ground operations is particularly striking in the context of reports regarding the redeployment of the 82nd Airborne Division and Marine expeditionary units toward Kharg Island. Trump’s silence on this matter can be interpreted in two ways: as an attempt to avoid political controversy ahead of the upcoming elections and the 250th anniversary of US independence, or as evidence of internal decision-making paralysis within the Oval Office. Meanwhile, Iran, sensing this hesitation, is intensifying attacks on the energy infrastructure of its neighbors, exemplified by strikes on tankers off the coast of Qatar and refineries in Saudi Arabia. There was also an attack on an Amazon data center in Bahrain and an aluminum production company in the UAE. Tehran’s actions have a clear objective: to place themselves in a better negotiating position by demonstrating that without a formal agreement with Iran, not a single barrel of oil will safely leave the Persian Gulf.

The Market Remains Blind: Why $150–$200 per Barrel is Becoming Realistic

Despite oil prices already crossing the psychological barrier of $100, the financial market continues to show a staggering lack of understanding regarding the scale of the impending crisis. Within the Trump administration, officials are quietly preparing for an “extreme scenario” in which the price per barrel reaches $150 or even $200. At such levels, the price of gasoline in the US would rise above $5 per gallon, which is absolutely unacceptable to the American consumer, for whom fuel purchases constitute a significant portion of spending. Although $150-per-barrel forecasts appear in the “black swan” scenarios of reputable institutions, the market seems to ignore such risks, and it does not appear that the Strait of Hormuz will be unblocked within a few days. The oil market is currently being stabilized by alternative routes, the release of part of the Strategic Petroleum Reserves, and additional barrels from Iran or Russia, upon which the United States has lifted sanctions. The decision to reduce sanctions and the increasing toleration of Russia as a primary supplier of commodities demonstrate the scale of the US administration’s lack of preparation for the worst-case scenario.

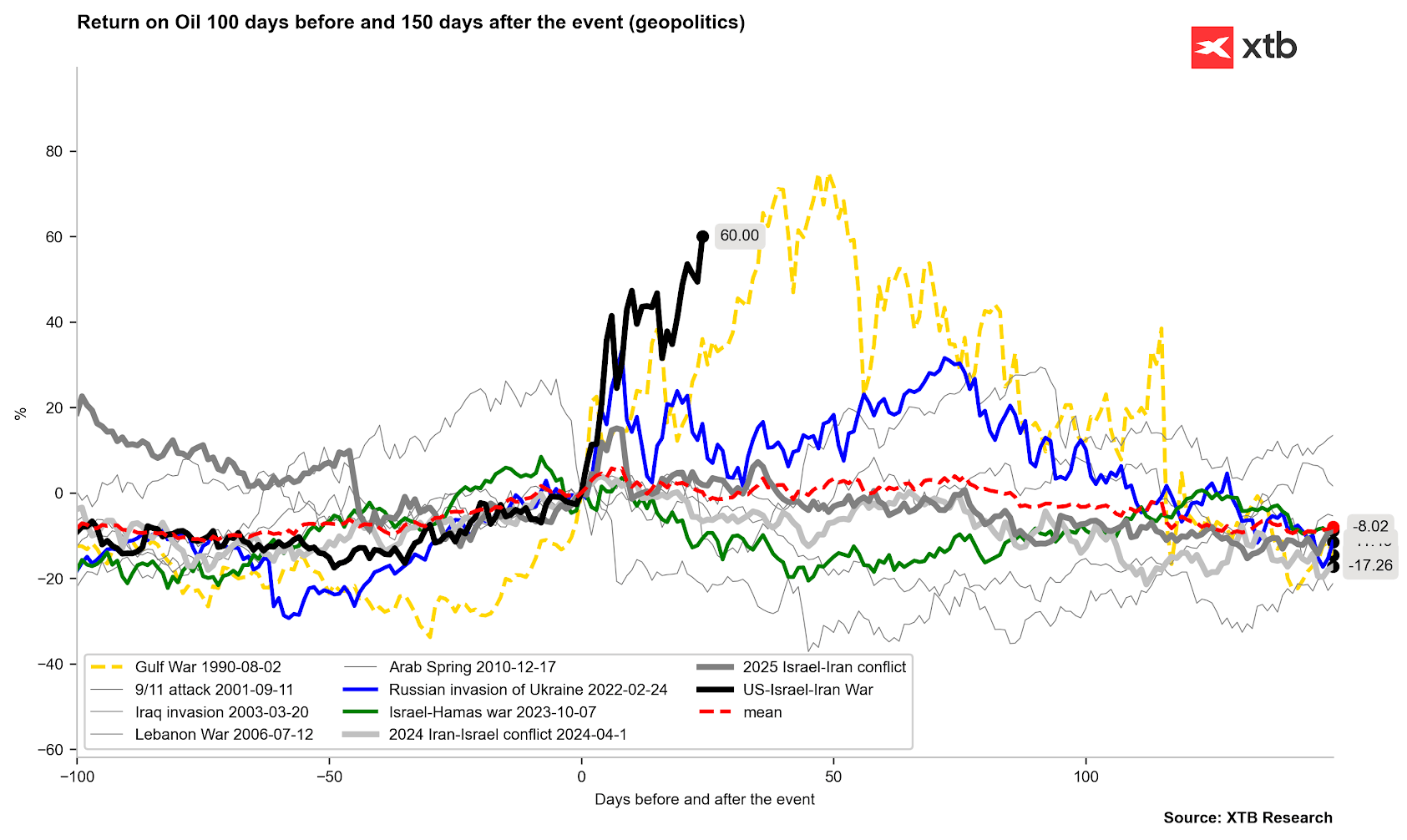

Oil prices are currently following the scenario of the oil crisis during the Persian Gulf War in the 1990s, when prices at their peak rose by up to 80% from the start of the war or by over 100%–120% from the start of the price hikes. Translating this to modern times would imply an increase to at least the $120–$130 per barrel range. Source: Bloomberg Finance LP, XTB.

Oil prices are currently following the scenario of the oil crisis during the Persian Gulf War in the 1990s, when prices at their peak rose by up to 80% from the start of the war or by over 100%–120% from the start of the price hikes. Translating this to modern times would imply an increase to at least the $120–$130 per barrel range. Source: Bloomberg Finance LP, XTB.

The current situation is unprecedented in modern history. Even the oil crises of 1973 and 1979 involved disruptions of approximately 6% and 4% of global supply, respectively. In the 1990s, during Operation Desert Storm, supply volatility was around 7%. Now, the offline production accounts for more than 10%, and the oil market is stabilized only by strategic reserves, which could be exhausted at any moment. Just as importantly, the world reached for its reserves even before the worst-case scenario materialized. What if it turns out that the Strait of Hormuz remains closed for months and, in the meantime, actual sinkings of tankers occur? The world is not ready for such a scenario.

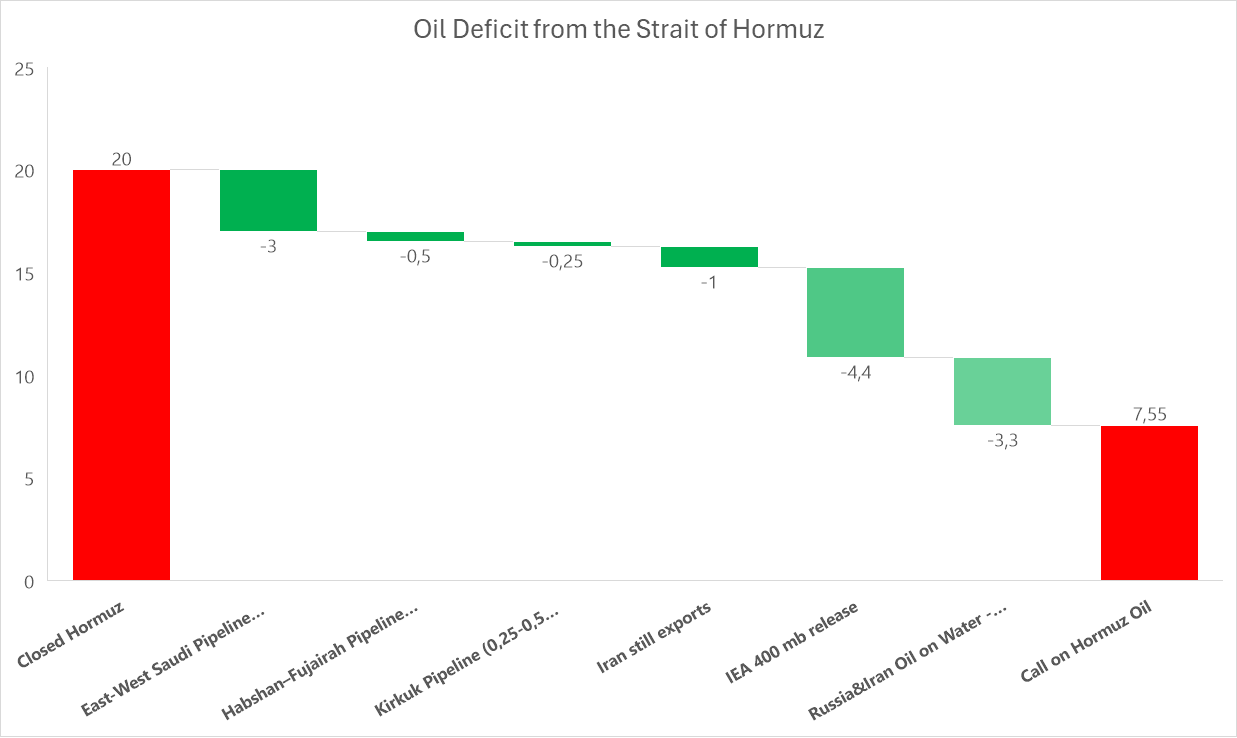

Currently, as much as 7–8 million barrels per day may be missing. Source: Kpler, Platts, S&P, Reuters, Bloomberg, XTB.

Currently, as much as 7–8 million barrels per day may be missing. Source: Kpler, Platts, S&P, Reuters, Bloomberg, XTB.

The Consumer at the Breaking Point: July 4th and the Shadow of the Midterms

For President Trump, the rise in fuel prices is not just an economic problem, but above all, an existential political threat. A price of $4 per gallon at US gas stations is already seen as a heavy burden on American families, but the $5 level is considered “unacceptable” and potentially capable of triggering mass social unrest. Trump has repeatedly boasted about lowering energy prices in the first year of his term, making the current jump of over a dollar per gallon in just one month exceptionally painful for his image.

The situation is worsened by the fact that the United States is preparing for the grand celebrations of the 250th anniversary of independence on July 4, 2026. The President’s planned “Salute to America 250″—a year of patriotic festivals set to culminate in Washington—could be overshadowed by record electricity and fuel bills. White House advisors fear that the frustration of voters, 60% of whom already express concern over the cost of living, will spill over into the results of the midterm elections in November.

What will China do?

In this dense weave of energy and political interests, the key point in geopolitical deliberations will be the meeting between Donald Trump and Chinese President Xi Jinping, scheduled for May 15 in Beijing. The visit, originally planned for March, was postponed precisely due to the outbreak of the war with Iran, which in itself demonstrates how much this conflict has destabilized the American foreign agenda. Trump would like China to join the effort to stabilize the situation in the Persian Gulf, but China is not reacting, even though their own access to oil is also heavily threatened.

Despite the fact that China draws approximately 50% of its oil from Persian Gulf countries, it finds itself in a relatively comfortable position regarding energy. Thanks to years of investment in renewable energy, the electrification of transport, and the diversification of imports (including from Russia and Central Asia), Beijing has increased its energy self-sufficiency to 85%. While the war hits Chinese industry, it simultaneously gives Xi Jinping powerful leverage in negotiations with Trump. Beijing could offer help in mediating with Tehran in exchange for concessions on Taiwan, the lifting of technological sanctions on semiconductors, or the loosening of export controls.

Although Trump wanted to meet Xi from a position of strength, at this moment it appears he is the one who should be asking for help. China may, however, offer the United States a “beautiful deal,” which on the surface might seem merely good, but which Donald Trump will be able to sell to voters as his own success. China remains in a “wait-and-see” mode, watching as the United States’ negotiating position diminishes day by day.

Arab Nations Plan Costly Emergency Investments

The situation is so critical that Arab countries, traditionally reliant on maritime transport, are beginning to consider scenarios that just a year ago were deemed economically absurd. The Financial Times highlights in its latest article intensive talks among Persian Gulf states regarding the construction of a new network of giant pipelines that would allow exports to be completely independent of the Strait of Hormuz. Saudi Arabia is best prepared for the crisis, as it already possesses a substantial East-West pipeline, through which it is already sending several million barrels to mitigate the impact of reduced revenues.

The problem is that pipeline infrastructure constitutes multi-year and extremely expensive projects. Even with the maximum utilization of existing lines, the global market still loses millions of barrels that physically cannot be sent overland. Moreover, these pipelines are becoming new targets for attacks: Iranian drones have already struck the Yanbu terminal, showing that changing the transport route does not eliminate the kinetic threat from Tehran.

How high can the price of oil go?

The oil market is already facing a shortage of several million barrels. The final market picture is difficult to estimate due to the use of stockpiles and previously sanctioned oil. Nevertheless, we can attempt to outline several realistic scenarios:

- Blockade of the Strait of Hormuz through April, followed by its partial reopening: In this scenario, oil consolidates at $100–$120 per barrel, US inflation rises by approximately 1 percentage point, but a catastrophic economic and market collapse is avoided. The market will quickly count on a return to normalcy, allowing indices and gold to begin a rebound before the end of the first half of the year.

- Immediate reopening of the Strait of Hormuz following an agreement: An unlikely but not impossible scenario. In this case, a large portion of the oil currently on ships is released to the world, and supply chains practically do not break down. Oil prices fall to $80 per barrel, indices rebound strongly, the dollar is heavily sold off, and interest rates will not be raised due to the temporary nature of inflation.

- Blockade of the Strait of Hormuz through the entire second quarter: Oil rebounds to $150–$180 per barrel, and stock index declines exceed 20% from recent local peaks. The risk of recession in Europe and a significant slowdown in other regions emerges. This could provide a buying opportunity in the stock market, as the world must force the reopening of the Strait of Hormuz.

- Further escalation, no talks with Iran, closure of the Strait of Hormuz extends through the summer: In this scenario, during moments of increased fuel demand, the oil price could rise to levels from the “black scenario”—prices of $200 per barrel. Adjusting for inflation, peak oil prices occurred in 2008 and amounted to over $200 per barrel. At such levels, we see a collapse of supply chains, a food-related crisis due to expensive fertilizers, and inflation becomes as major a problem as it was in the United States during the 1970s.

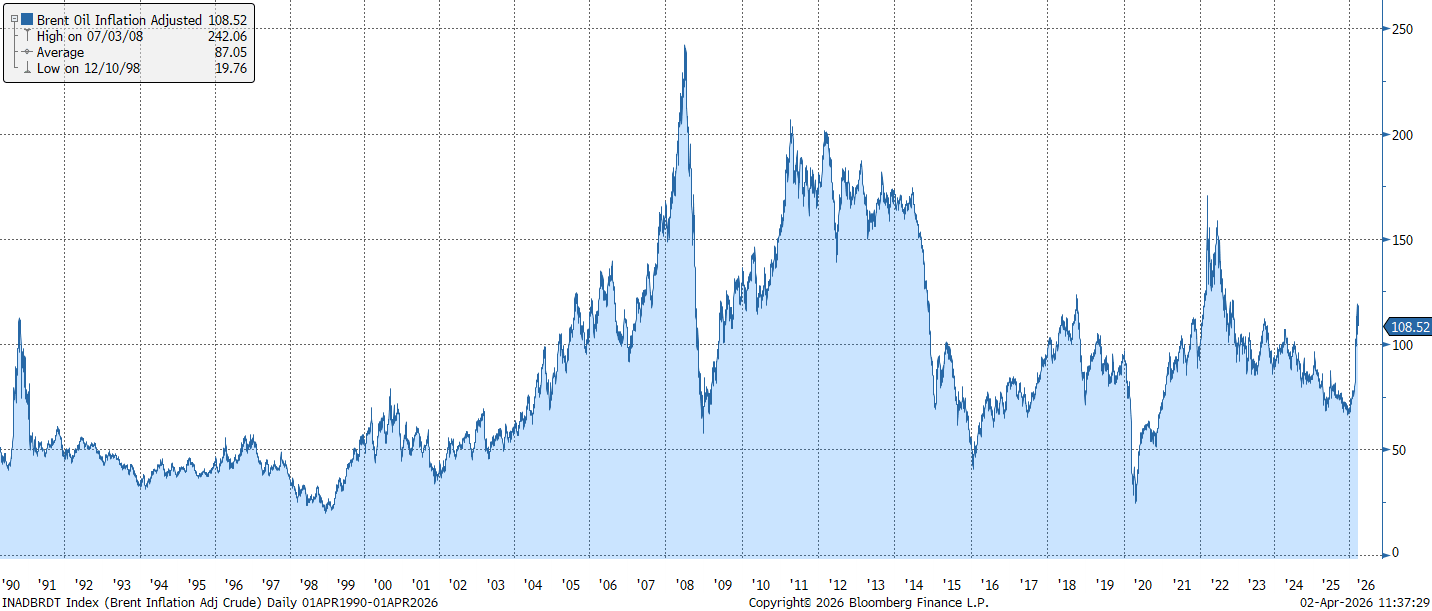

Adjusting the oil price for inflation, $200 levels were already recorded in 2008. The inflation-adjusted price shows how relatively low we still are, given the scale of the crisis. Source: Bloomberg Finance LP, XTB.

Adjusting the oil price for inflation, $200 levels were already recorded in 2008. The inflation-adjusted price shows how relatively low we still are, given the scale of the crisis. Source: Bloomberg Finance LP, XTB.

A Market in Suspense

In conclusion, Donald Trump’s address on April 1, 2026, must be considered a strategic communication failure. The President attempted to sell the public an image of a victorious war, ignoring the fact that from an economic perspective, this war is currently being lost miserably at gas stations and oil export terminals. The lack of a concrete plan to unblock the Strait of Hormuz, combined with the intensification of attacks by Iran and the looming exhaustion of strategic reserves, creates an explosive mix that could drive oil prices to the $150–$200 level before the July 4th celebrations of the US 250th anniversary.

The market, though still exhibiting some inertia, is beginning to realize that the Trump administration does not control the situation as it claims. The real test will occur on May 15 in Beijing. If Trump fails to negotiate a de-escalation mechanism with Xi Jinping that forces Iran to open the strait, American consumers may welcome Independence Day not just with $5 gasoline, but with energy rationing that will forever change the perception of United States “energy dominance.” The crisis that the market did not want to see is already knocking at the door, and the President’s address only confirmed that no one inside the White House holds the key to stopping it.

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.