S&P 500 — US Large Cap Index

S&P 500 — US Large Cap Index FTSE 100 — UK Blue Chips

FTSE 100 — UK Blue Chips Euro Stoxx 50 — Eurozone Leaders

Euro Stoxx 50 — Eurozone Leaders DAX 40 — German Equities

DAX 40 — German Equities CAC 40 — French Market Index

CAC 40 — French Market Index Nikkei 225 — Japan Benchmark

Nikkei 225 — Japan Benchmark Hang Seng — Hong Kong Index

Hang Seng — Hong Kong Index Shanghai Composite — China Mainland

Shanghai Composite — China Mainland ASX 200 — Australian Market

ASX 200 — Australian Market TSX Composite — Canada Index

TSX Composite — Canada Index Nifty 50 — India Large Cap

Nifty 50 — India Large Cap STI Index — Singapore Market

STI Index — Singapore Market KOSPI — South Korea Index

KOSPI — South Korea Index Bovespa — Brazil Equities

Bovespa — Brazil Equities JSE Top 40 — South Africa Index

JSE Top 40 — South Africa Index IPC Index — Mexico Market

IPC Index — Mexico MarketPreview – Netflix stock up 18% since the start of 2026 📊 Q1 earnings in focus

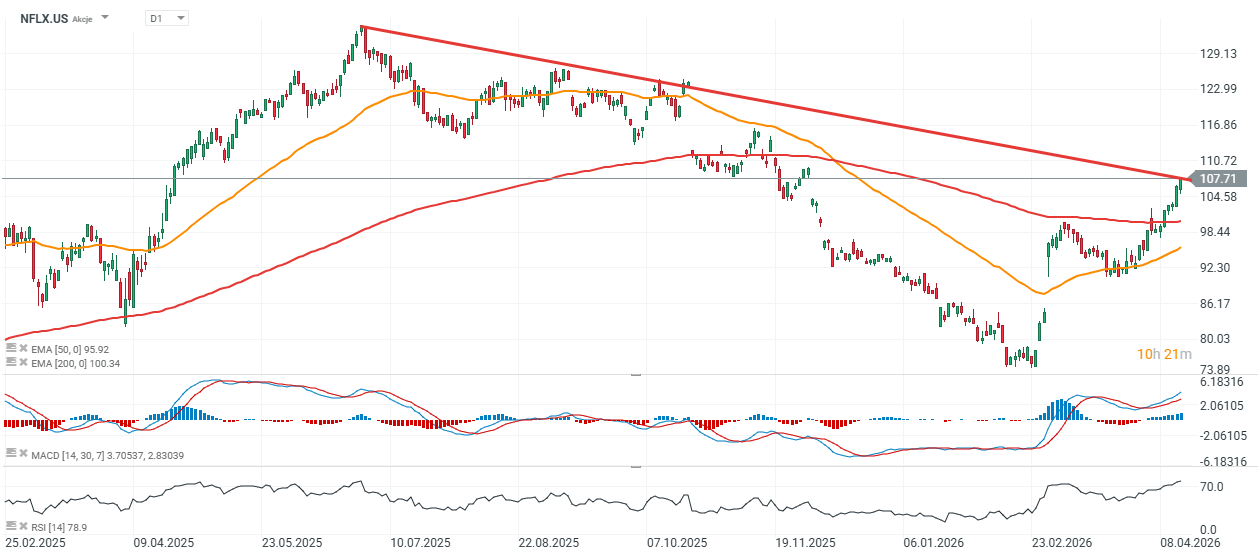

Netflix (NFLX.US) will report its Q1 2026 results after the market close on April 16. The company enters the release with strong share price momentum and elevated investor expectations, meaning that merely meeting consensus may not be enough to sustain the rally. The key question is not only whether Netflix delivers on revenue and earnings per share, but whether it can confirm the durability of its two core growth engines: subscriptions and advertising. Wall Street expects revenue of approximately $12.16–12.20 billion, implying around 15% year-over-year growth. Consensus EPS stands at roughly $0.76–0.78. The market is therefore pricing in a solid quarter, and with the stock already up more than 18% year-to-date, the focus shifts from simply “beating estimates” to the quality of growth and the outlook for the coming quarters. Netflix Q1 2026 earnings: market looking for confirmation of growth durability Netflix will release its Q1 2026 results after the close on April 16. The company enters the report with strong market momentum, with shares rising significantly year-to-date. Additional support for sentiment came from the company’s decision to walk away from a planned transaction involving Warner Bros. Discovery, which resulted in a $2.8 billion termination fee. However, for investors, the one-off effect is less important than whether Netflix can confirm the sustainability of its growth model in an environment of higher pricing, increasing reliance on advertising, and elevated full-year expectations. Consensus points to a solid quarter, but expectations are high Wall Street expects revenue in the range of $12.16–12.20 billion, representing roughly 15% year-over-year growth. Consensus EPS is estimated at $0.76–0.78. This setup suggests the market is already anticipating a strong quarter, meaning that simply meeting expectations may not be sufficient to drive a positive share price reaction. The focus will be on growth quality, monetization structure, and management commentary on upcoming quarters. Analyst sentiment also remains constructive, with the majority of recommendations still positive and price targets from major brokerages above current trading levels. Subscriber growth after price hikes will be the first major test The most important area of the report will be the pace of paid subscriber growth following recent price increases. Netflix has successfully combined scale expansion with improved monetization in recent quarters, but the market now wants to see whether this model remains resilient after the March pricing changes. Commentary on churn and the regional distribution of growth will be particularly important. Investors will look for confirmation that international markets—especially Asia and other high-growth regions—continue to offset the more mature U.S. market. If the company demonstrates resilience in its user base despite higher prices, it would support the narrative of continued revenue expansion. Advertising is becoming the second growth pillar The second key focus will be the development of the advertising segment. For the market, advertising is no longer a secondary feature of the subscription model but is increasingly viewed as a second core pillar. Investors will assess not only the growth rate of advertising revenue, but also the adoption of the ad-supported tier and its impact on ARPU and the overall customer mix. If management shows that advertising is scaling without materially weakening the quality of subscription revenues, this could support further valuation expansion. Conversely, weaker commentary on advertising could raise concerns that current expectations are too optimistic. In this context, investors will also monitor the expansion of live content, which may enhance the attractiveness of Netflix’s advertising offering. During the quarter, the company expanded its live programming, including streaming a BTS concert from Seoul and the 2026 World Baseball Classic. The market will evaluate whether such content can support further advertising revenue growth and strengthen Netflix’s positioning with advertisers. Margins and cost discipline remain central to the investment case The third area of focus will be operating profitability and cost control. Netflix guided for an operating margin of around 32% for the quarter, and investors will assess whether the company can maintain cost discipline while continuing to fund a high level of content investment. This is critical, as the current investment thesis is no longer based solely on scale growth, but on the company’s ability to translate that scale into higher cash flow and more predictable profitability. A margin beat could reinforce positive sentiment, while signs of cost pressure would likely weigh on the stock. It will also be important whether management signals a continued balance between content investment and profitability. The company has previously indicated that content and advertising will be the main drivers of growth, and the market will evaluate whether this strategy continues to support financial performance without significantly increasing cost pressure. Full-year guidance may matter more than the quarter itself Ultimately, the most important element of the report may not be the first-quarter results themselves, but management’s commentary on full-year 2026 guidance. Consensus currently assumes revenue growth in the range of 12–14% for the year, and the market will be highly sensitive to any indication of an upward revision. Given the strong share price performance and elevated expectations, it is likely that forward guidance—rather than the quarterly figures—will drive the post-earnings reaction. A failure to raise guidance, even with solid Q1 results, could trigger profit-taking. The market is looking for confirmation, not just solid numbers From a market perspective, this is a high-stakes report. Netflix needs to demonstrate not just growth, but that growth remains durable after price increases, that advertising is scaling as expected, and that there is room to improve full-year expectations. If these elements are confirmed, the company may maintain its leadership within the media sector. If not, the high bar set by current expectations could quickly weigh on the stock. In practical terms, this report will test whether Netflix can simultaneously raise prices, expand its paying subscriber base, scale advertising, and sustain strong profitability. At current valuation levels and after a strong run in the share price, investors are no longer looking for a solid quarter alone. They are looking for confirmation that further growth is achievable and that the existing valuation premium remains justified. Netflix stock technical setup Netflix shares are trading around 10% above the 200-day moving average (EMA200), which may act as a key support level in a downside scenario. The stock has recently approached resistance near $108. A breakout above this level could signal an acceleration of the uptrend, while a move below $100 would suggest weakening medium-term momentum.

Source: xStation5

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.